What changes for companies, directors and creditors?

Directive (EU) 2026/799 of the European Parliament and of the Council of 30 March 2026 (the Directive”) was published on 1 April 2026. It establishes a framework for the minimum harmonisation of certain substantive aspects of insolvency law in Member States. The Directive is also relevant to the European Economic Area.

- Entry into force: 21 April 2026

- Deadline for transposition: 22 January 2029

- Member States may maintain or adopt national provisions that offer greater protection to creditors, provided they are compatible with EU law.

1. Context and objectives

The Directive forms part of the Capital Markets Union agenda. The main objective is to reduce divergences between national insolvency laws that affect legal certainty and the predictability of insolvency proceedings outcomes, as well as the attractiveness of cross-border investment. Specifically, it seeks to mitigate the obstacles to the free movement of capital and freedom of establishment that arise from regulatory differences.

Rather than full harmonisation, the European legislature has opted for a selective approach, focusing on areas critical to the efficiency and economic value of insolvency proceedings.

2. Scope of application

The Directive applies to collective insolvency proceedings involving all or a significant proportion of the debtor’s creditors. It excludes preventive restructuring schemes (such as the PER - Special Revitalisation Process in Portugal), credit institutions, insurance companies, and other financial entities subject to special supervision. Individuals who do not carry out business activities are also excluded.

3. Main harmonised areas

The Directive establishes minimum rules in five key areas:

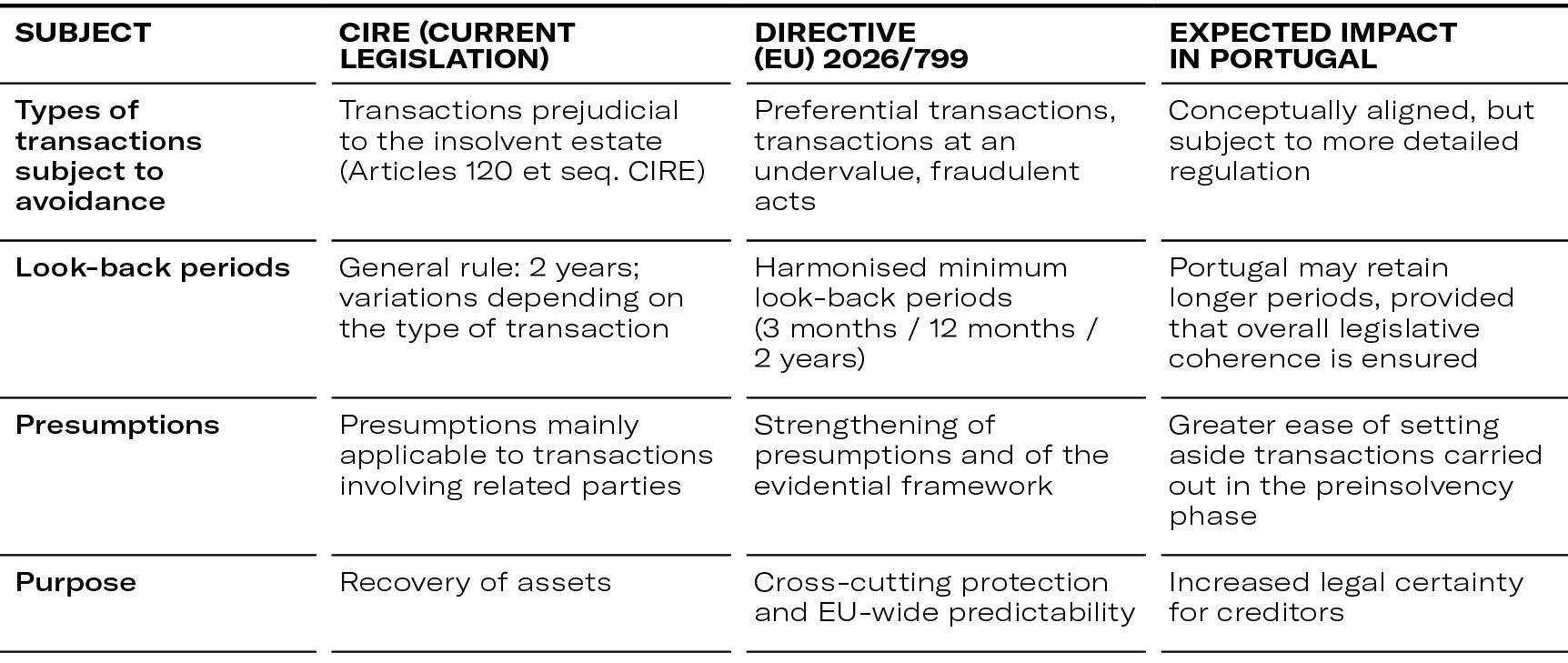

- Avoidance actions: it introduces minimum rules under which transactions detrimental to creditors may be declared void, voidable or unenforceable, defining look-back periods and presumptions, including in transactions involving related parties.

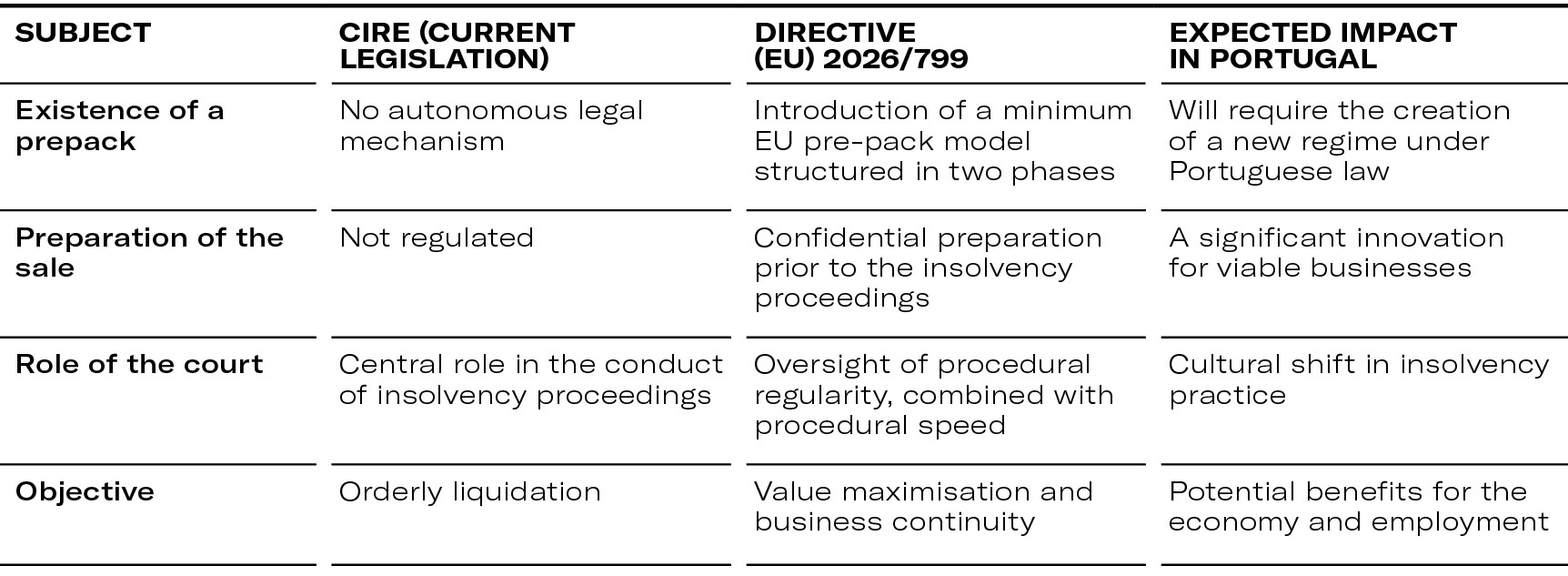

- Pre-pack procedures: it provides a new model for the sale of viable businesses or assets prepared prior to the formal opening of insolvency proceedings to maximise their value.

- Duty to file for insolvency: it sets out minimum requirements regarding the duty of directors to file for insolvency in a timely manner.

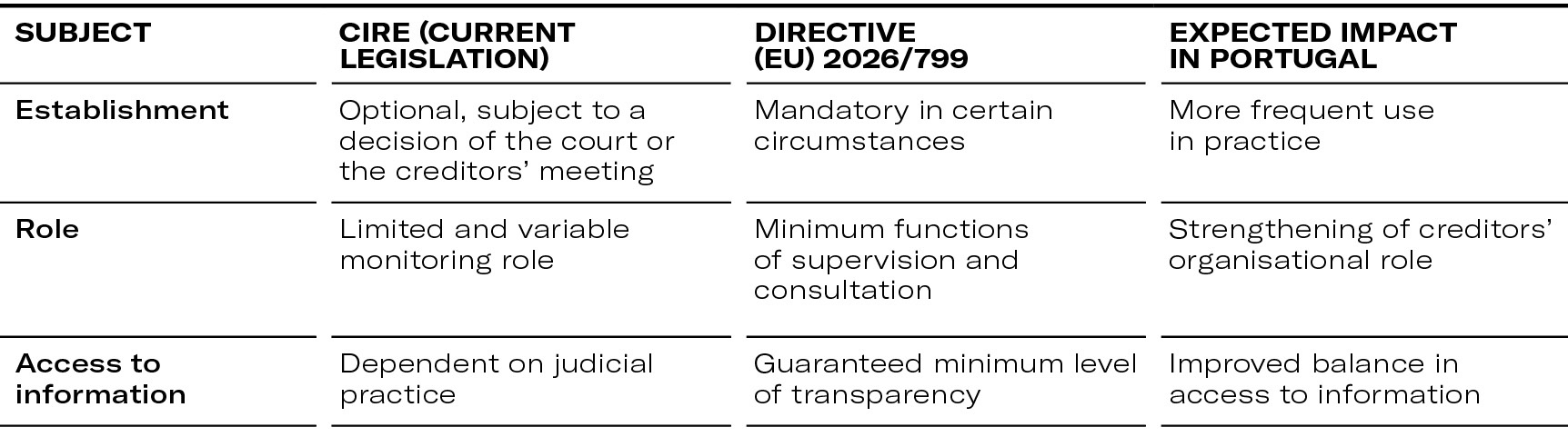

- Creditors’ committees: it mandates their existence in certain circumstances, thereby strengthening their supervisory and monitoring role in insolvency proceedings.

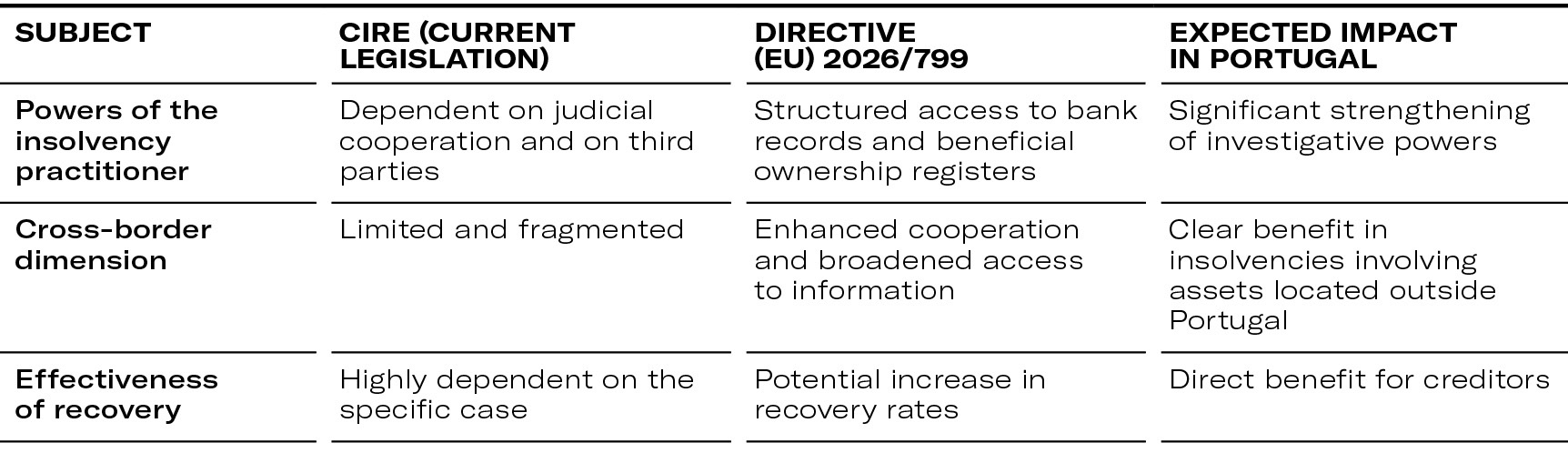

- Asset tracing: it strengthens the powers of insolvency practitioners to access relevant information, including bank records and beneficial ownership registers, in both domestic and cross-border contexts.

4. Relevance and impacts of Directive (EU) 2026/799 in Portugal

The Directive represents a further step towards the European convergence of insolvency law and will require a critical assessment of domestic legislation, particularly the Insolvency and Corporate Recovery Code (“CIRE”).

The Portuguese legal system already provides solutions in several areas that are similar to those now required by the Directive. However, legislative adaptation will be necessary in other areas. This presents an opportunity to modernise and improve Portuguese insolvency legislation.

The harmonisation of certain aspects of insolvency law will have significant direct and indirect effects in Portugal. There are implications for various stakeholders, including companies (debtors), directors, and creditors.

4.1. Impact on companies (debtors)

4.1.1. Greater predictability and preinsolvency scrutiny

Companies should be aware that certain transactions, such as preferential payments, transfers to related parties, and sales below market value, may be challenged on the basis of minimum European criteria.

Practical impact in Portugal:

Although the CIRE already provides for avoidance actions for the benefit of the insolvent estate, the Directive requires:

- Clearly defined look-back periods.

- Strengthened presumptions in transactions involving close relationships.

- Greater consistency in proving losses to creditors. This may lead to more cautious management in preinsolvency situations.

This may lead to more cautions management in preinsolvency situations.

4.1.2. Greater predictability and preinsolvency scrutiny

The Directive establishes a framework for prenegotiated sale procedures (pre-packs), which are not recognised as a separate legal concept under Portuguese law. The aim of this mechanism is to enable:

- The preparation of the sale prior to insolvency.

- Rapid execution of the sale following the opening of insolvency proceedings.

- The preservation of value and jobs.

Practical impact in Portugal:

For viable companies facing imminent insolvency, the prepack could become:

- A faster alternative to traditional liquidation.

- An attractive instrument for investors.

- A complement the to the PER (Special Revitalisation Process) and the RERE (Out-of-court Corporate Recovery Scheme), although it is distinct from them.

4.2. Impact on directors

4.2.1. Strengthening of the duty to file for insolvency

The Directive sets out rules regarding the duty of directors to file for insolvency in a timely manner. The aim is to prevent an increase in liabilities and the dissipation of assets.

Practical impact in Portugal:

Although this duty already exists under the CIRE, transposition of the Directive may:

- Narrow the definition of the CIRE concept of “appropriate time”.

- Strengthen duties of care in the preinsolvency phase.

- Increase directors’ exposure to civil and, potentially, administrative liability.

These rules emphasise the importance of documented and prudent management when companies are experiencing financial difficulties. They reduce the margin of discretion and increase directors’ exposure to potential liability.

4.2.2. Greater transparency and cooperation

The strengthening of mechanisms for tracing and recovering assets means that directors should expect stricter monitoring of asset flows and greater investigative powers for insolvency practitioners.

4.3. Impact on creditors

4.3.1. Strengthening of the role of creditors’ committees

The Directive requires the establishment of such committees in certain circumstances, giving them effective monitoring, supervisory and advisory functions in insolvency proceedings.

Practical impact in Portugal:

Under Portuguese legislation, creditors’ committees already exist, but they are not used consistently. The transposition of the Directive may:

Make their establishment more frequent.

- Strengthen their powers to obtain information.

- Increase creditors’ influence over the conduct of the proceedings.

4.3.2. Higher potential debt recovery rates

Harmonising legal challenges and strengthening asset tracing, including access to bank and beneficial ownership records, increases the likelihood of:

- Identifying hidden assets.

- Recovering fraudulently transferred assets.

- Reducing information asymmetries

For institutional creditors and investors, this means greater predictability of recoverable value and lower legal risk in cross-border insolvencies.

5. Comparative Tables - CIRE V Directive (EU) 2026/799

5.1. Avoidance actions (avoidance of transactions for the benefit of the insolvent estate)

5.2. Prepack procedures

5.3. Duty to file for insolvency and directors' duties

5.4. Creditors' commitee

5.5. Asset Tracing

6. Final Remarks

The CIRE is already largely in line with several principles of the Directive, particularly in the area of avoidance actions. The most significant changes for Portugal will therefore be:

- The introduction of a prepack procedure.

- The effective strengthening of directors’ duties in the preinsolvency context.

- The consolidation of the role of creditors’ committees.

- The expansion of asset tracing mechanisms.

The Directive provides an opportunity to modernise and streamline Portuguese insolvency law, thereby enhancing market and corporate financing confidence.